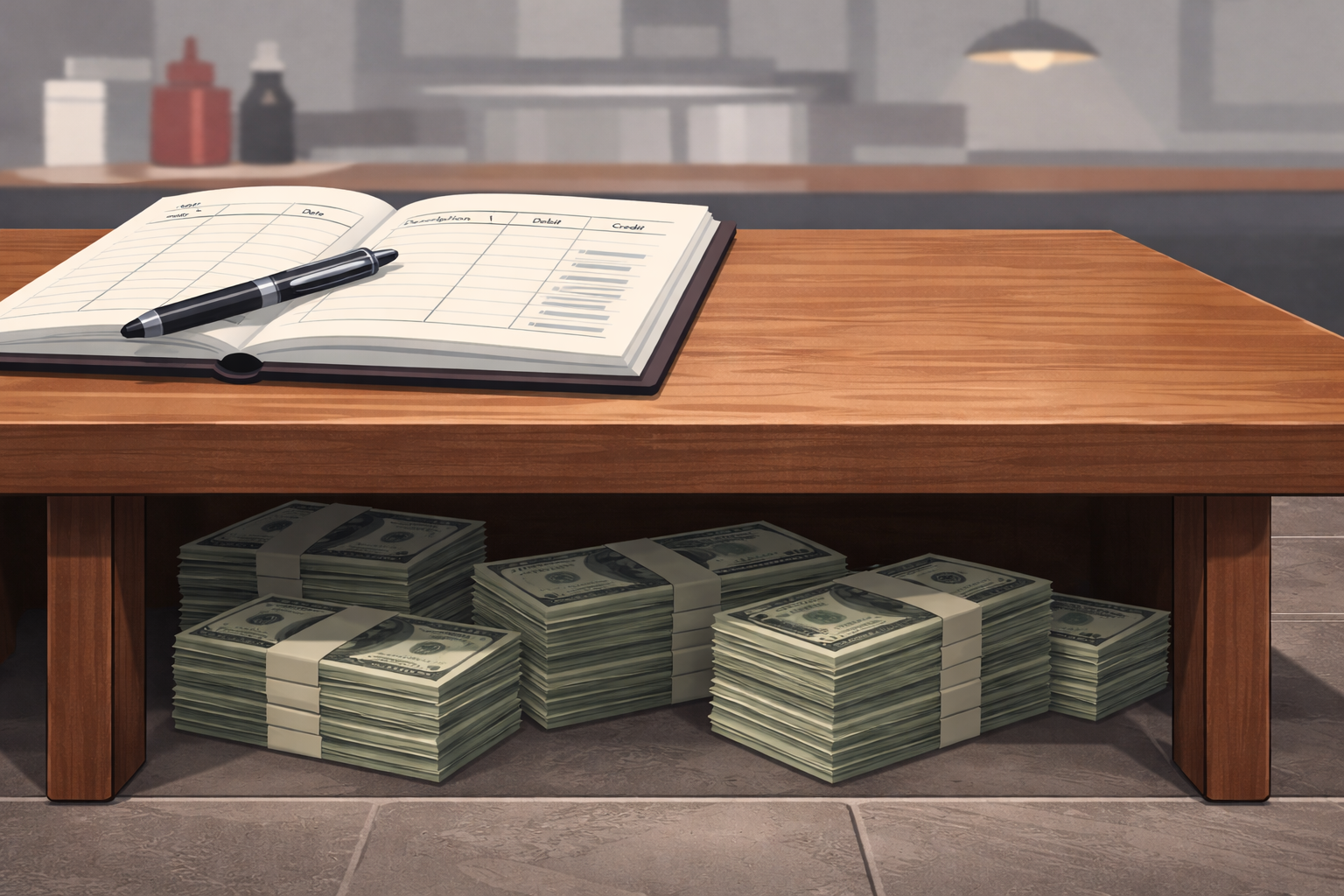

When cash never hits the books, can an accounting still deliver meaningful relief? A recent decision offers answers—and warnings.

Continue Reading Can an Equitable Accounting Find the Missing Cash?

When cash never hits the books, can an accounting still deliver meaningful relief? A recent decision offers answers—and warnings.

Continue Reading Can an Equitable Accounting Find the Missing Cash?

The equitable accounting claim in business disputes has experienced a resurgence. This week’s post explores the recent developments reinforcing the potency of this once-fading legal remedy.

Continue Reading Strength in Numbers: The Resurgence of the Accounting Claim in Business Divorce Litigation

In what he described as “the aftermath of what had been an amicable business divorce,” New York County Commercial Division Justice Joel Cohen discusses several interesting and novel limitations on New York’s cause of action for an equitable accounting.

Continue Reading But What of the Equitable Accounting?

In litigation between co-owners of private business entities, a claim against the controllers for an equitable accounting is different from a claim seeking access to books and records — or is it? Get the answer in this week’s New York Business Divorce.

Continue Reading Equitable Accounting vs. Access to Books and Records: Don’t Confuse Them