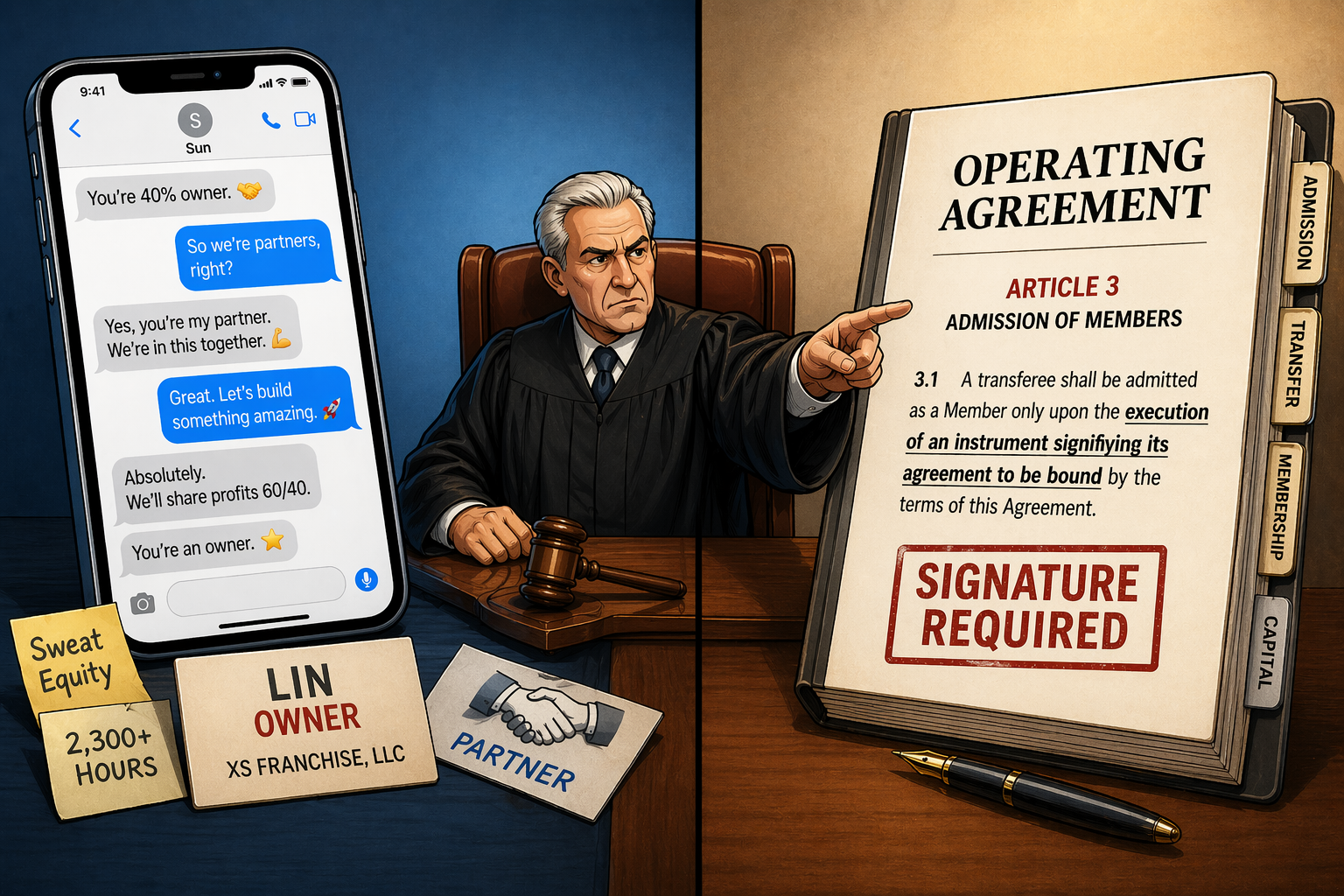

Can an operating agreement require majority approval before a minority member may sue derivatively? A recent Delaware decision warns against letting authority provisions swallow the derivative claim whole.

Continue Reading The Derivative Claim and the Majority Approval Trap