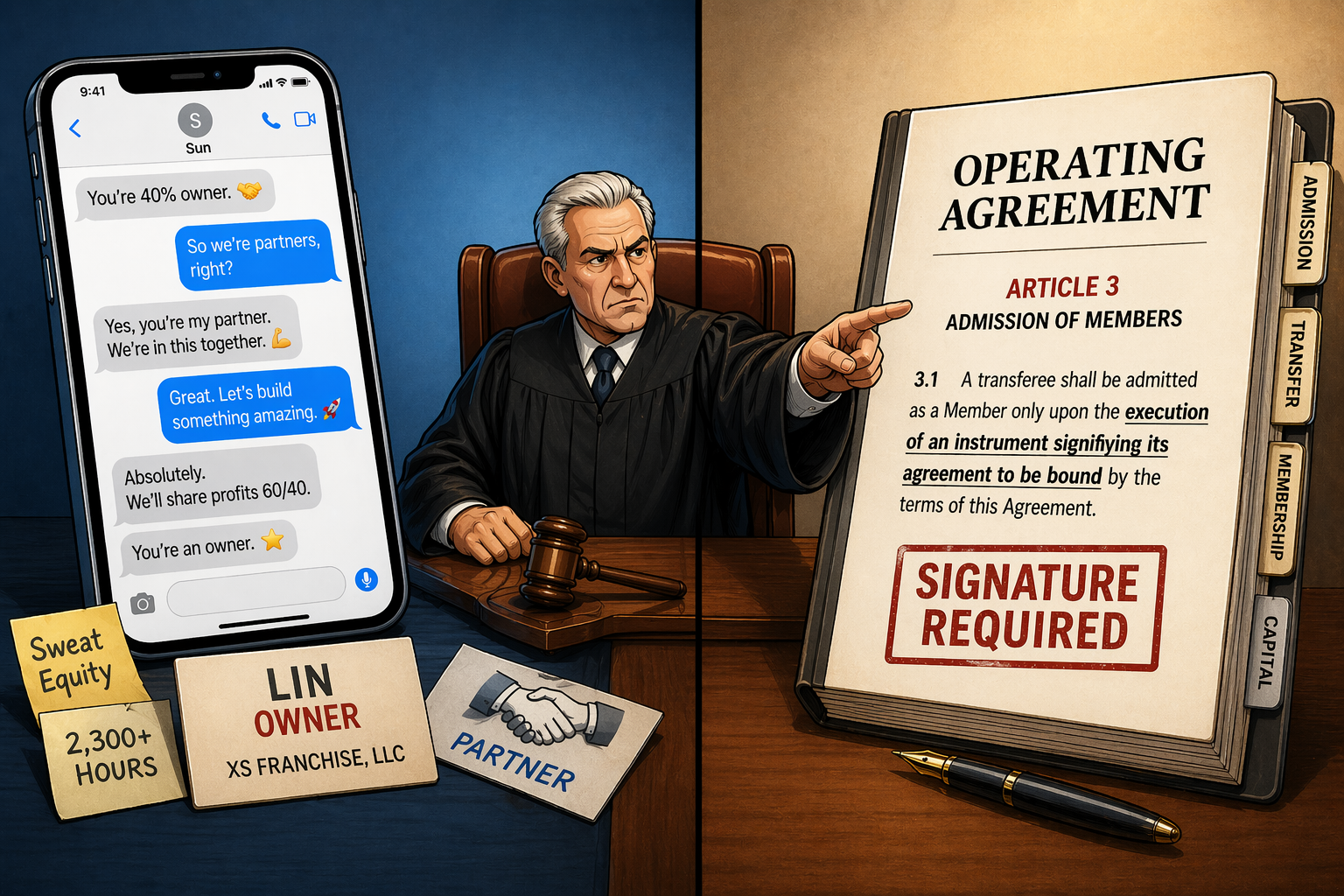

A recent Second Department decision reminds business divorce litigants that while K-1s may be powerful evidence of an economic interest, they cannot substitute for compliance with a partnership agreement’s formal admission requirements.

Continue Reading Tax Partner, Not True Partner: The Limits of K-1s in Business Divorce Litigation